The information shown on the statement of account depends on each financial situation. The explanations given in the statement examples below answer the most frequently asked questions.

Statement of account sent to an individual who is not self-employed

Here's an example of a statement of account sent to an individual who is not self-employed. Click on the question mark for the information you want to see.

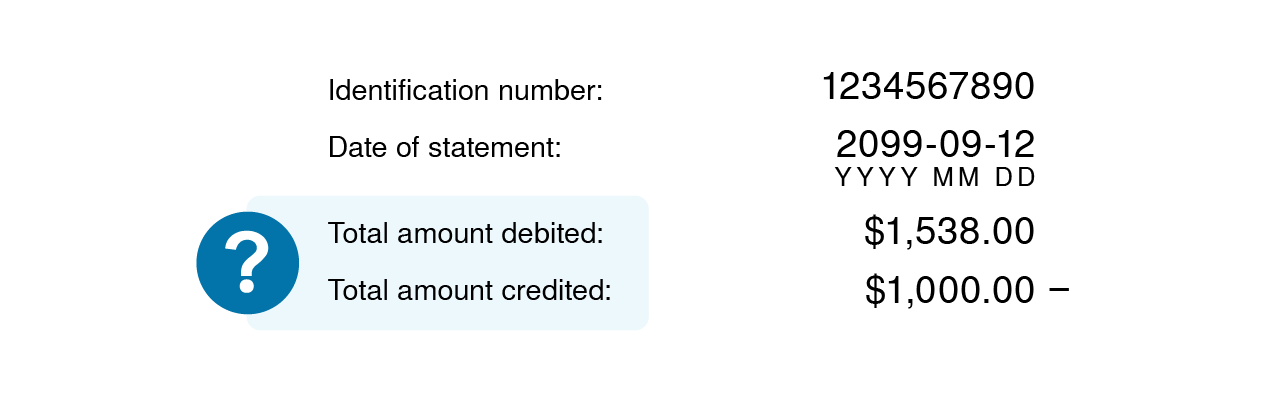

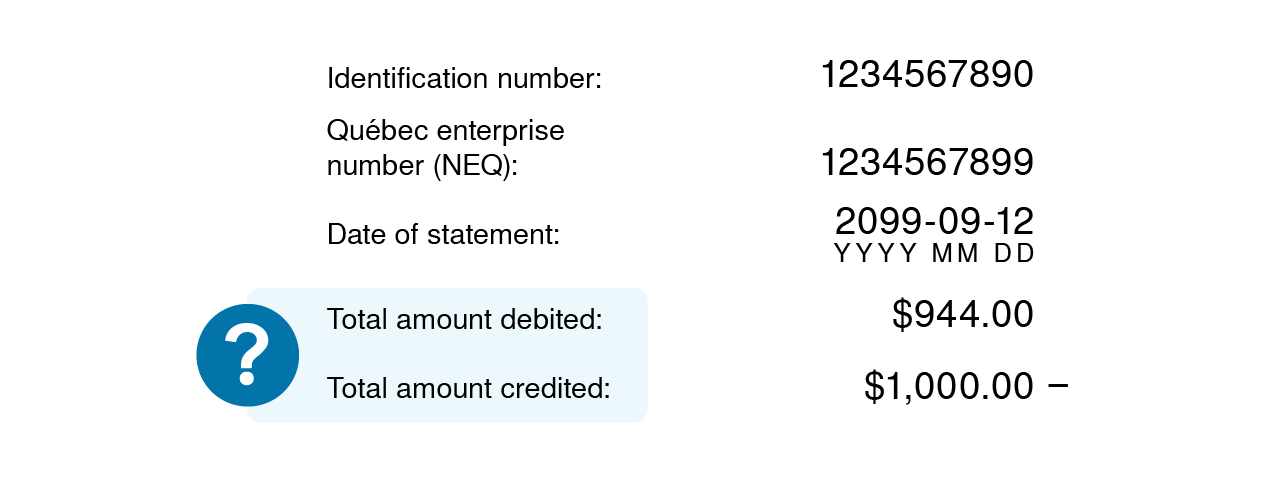

Total amount debited

Total balance you must pay.

Total amount credited

Instalment payment amount that you've remitted for your return that we have not yet received or processed. This may also be an amount related to any other credit that was not yet accounted for, such as overpayments or a credit that was misallocated.

Although tax credits you're entitled to are entered in the “Amount credited” column, they are not included in your total amount credited (top right).

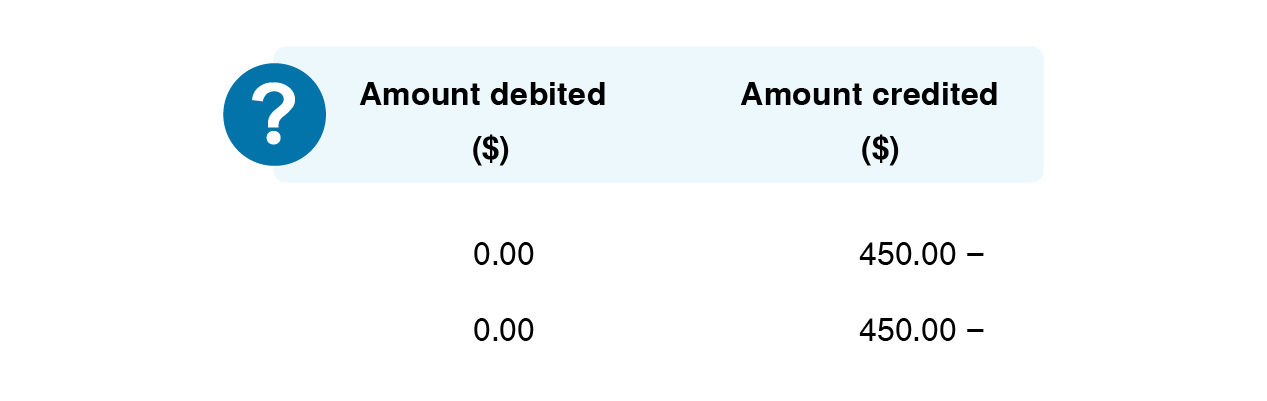

Amount debited column

We use the amounts shown in this column to calculate your total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are added to the balance you must pay.

Amounts followed by a minus sign (-) are subtracted from the balance.

Amount credited column

This column has no direct bearing on the “Amount debited” column, and we do not include the amounts in it when calculating your total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are paid to you.

Amounts followed by a minus sign (-) reduce the balance of your “amount credited” to $0 if payments were made to you.

If you make instalment payments, they will be followed by a minus sign (-) and, when your notice of assessment is issued, they will be deducted from your balance.

The process of applying all instalment payments you've made for a given taxation year to the payment of your balance. We do this when we issue your notice of assessment for your income tax return. The process allows us to reduce your “amount credited” to zero.

“Application” is used in other accounting entries that may appear in a statement of account. Generally speaking, it means processing an amount to reduce the amount credited to zero.

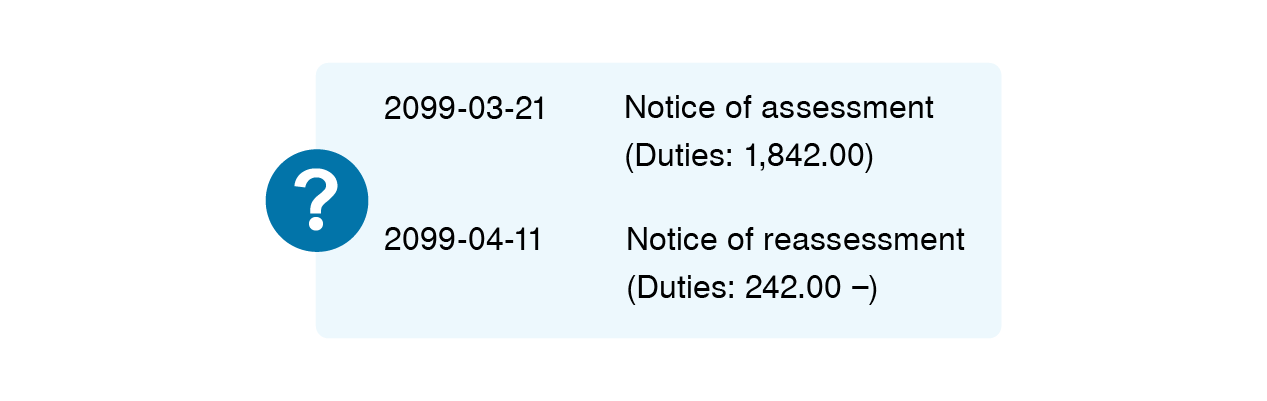

Notice of assessment

Paper or electronic document that we issue after reviewing an income tax return you filed. It shows:

the calculation of income tax and any interest and penalties you must pay for a given taxation year, as well as amounts you've already paid for the year

the balance you must pay or the refund you're entitled to for the return for the taxation year

Notice of reassessment

Paper or electronic document that we issue, for example, after you make a request to change your income tax return or after your file was audited. The notice of reassessment amends your previous notice of assessment. It shows:

the revised calculation of income tax and any interest and penalties that you must pay for a given taxation year, as well as amounts that you've already paid for the year

the adjusted balance you must pay or the adjusted refund you're entitled to for your return for the year

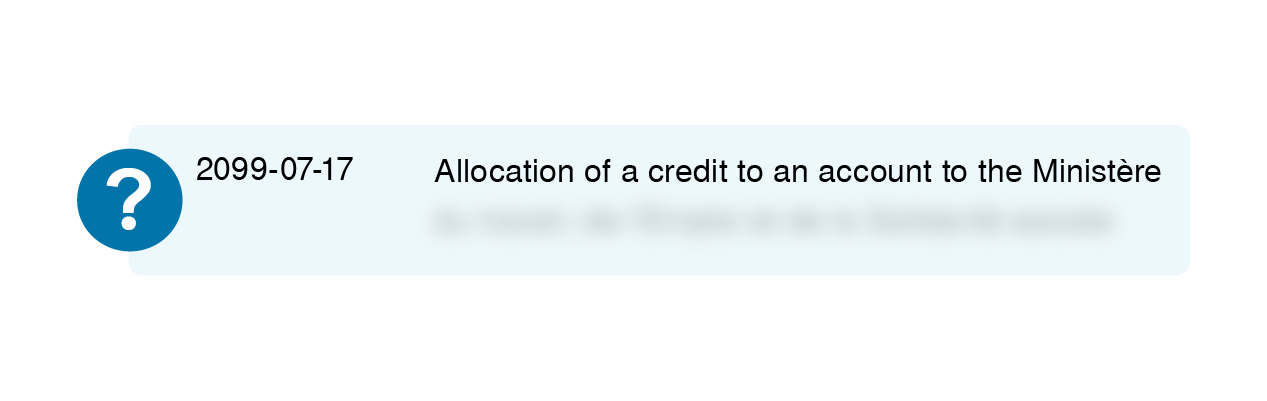

Allocation of a credit to an account

Use of a tax credit you were owed to reduce or pay a debt you have with us or with another Québec government department or body.

“Allocation” is used in other accounting entries that may appear in a statement of account. In all cases, it means use of an amount owed to you to reduce or pay a debt you owe.

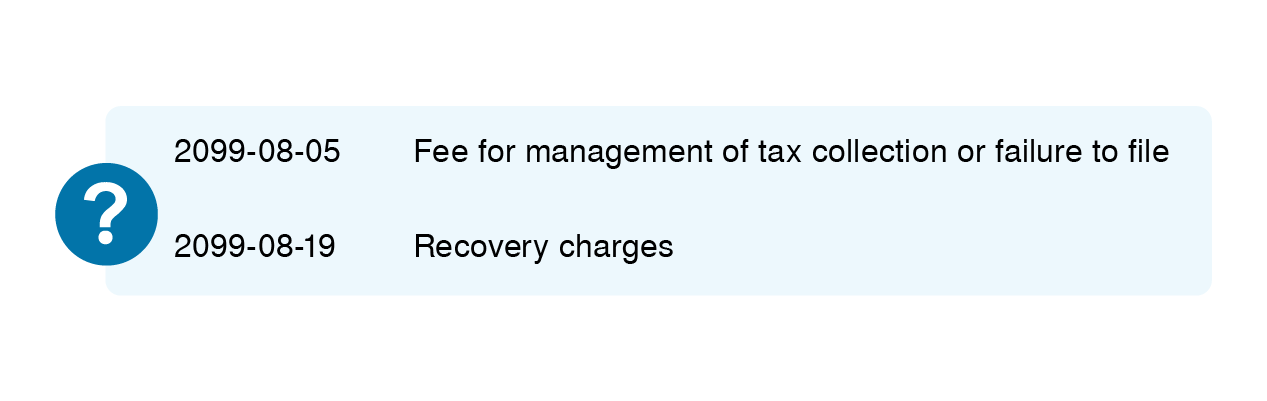

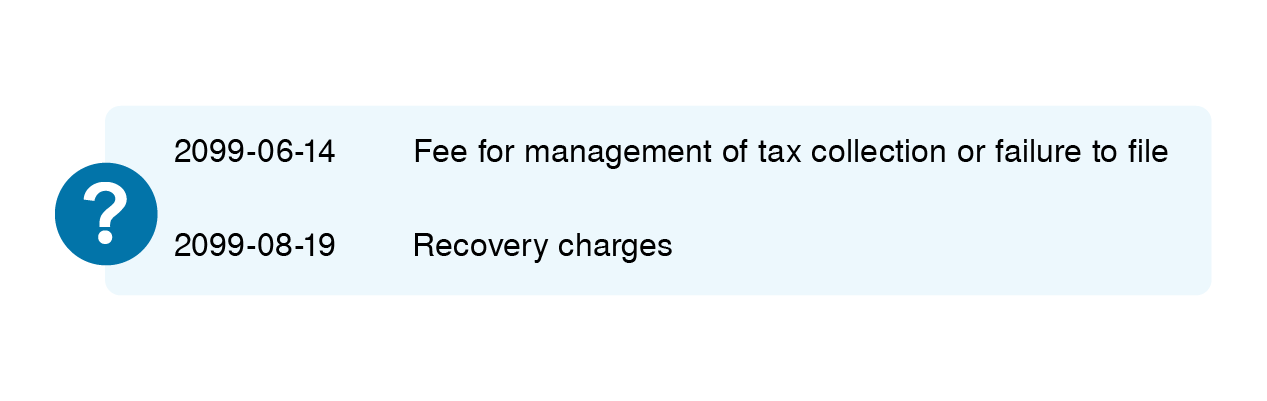

Fee for management of tax collection or failure to file

Fixed fee charged to open your collection file.

Recovery charges

Fees charged to you if we have to take administrative or legal measures to collect an amount you owe us.

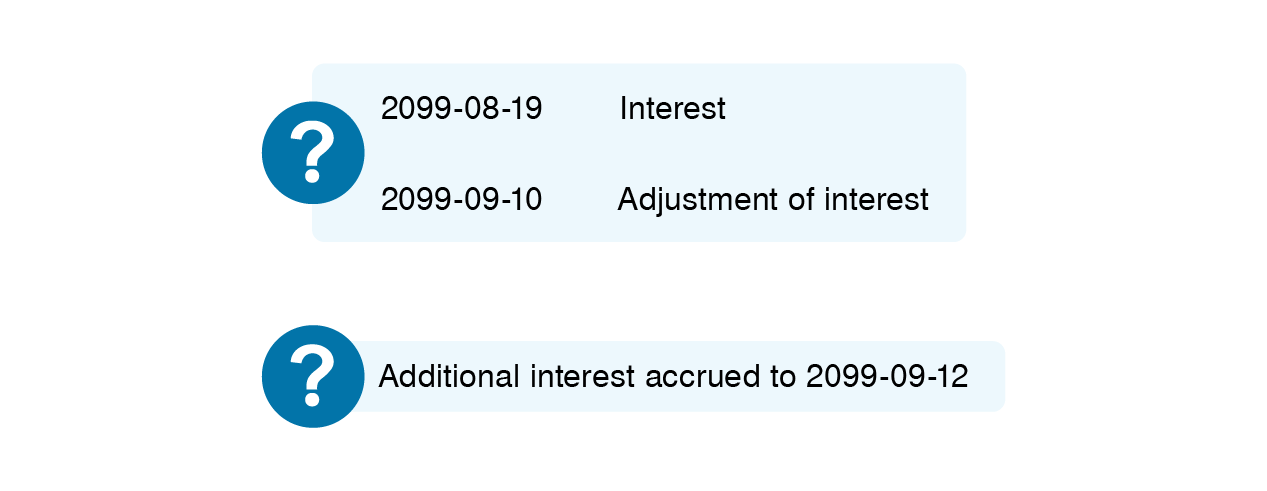

Interest

Amount added to your balance, at the rate set by law, for each day after the payment deadline.

Adjustment of interest

Recalculation of interest based on payment (partial or full) of your balance or application of a credit to the balance.

Additional interest

Additional interest added to the interest already calculated daily on the balance you haven't paid within the required timeframe.

Statement of account sent to a self-employed person (individual in business)

Here's an example of a statement of account sent to a self-employed person (individual in business). Click on the question mark for the information you want to see.

Total amount debited

Total balance you must pay.

Total amount credited

Instalment payment amount that you've remitted for your various returns that we have not yet received or processed. This may also be an amount related to any other credit that was not yet accounted for, such as overpayments or a credit that was misallocated.

Although tax credits you're entitled to are entered in the “Amount credited” column, they are not included in your total amount credited (top right).

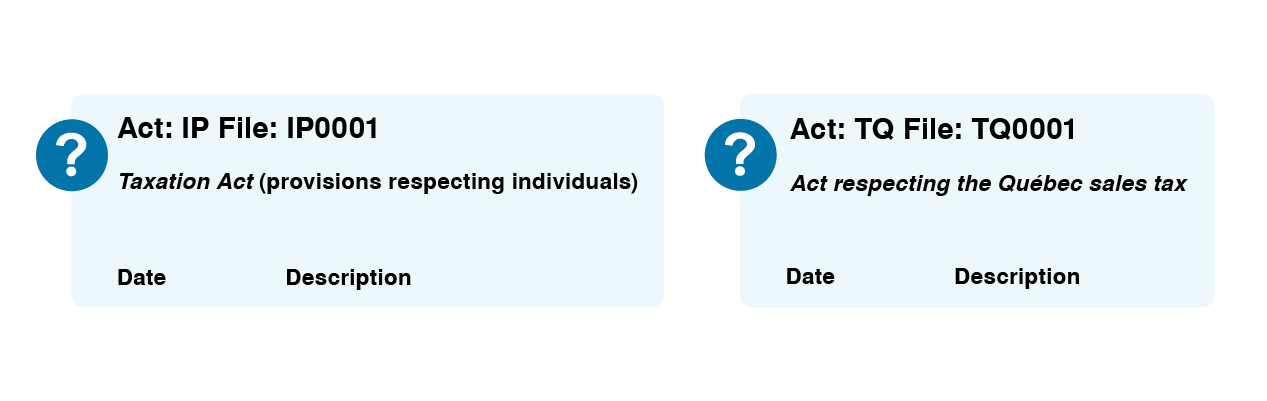

Act, file number respecting the act and year or period

Act under which you are required to pay a balance owed or are entitled to a refund, and file number respecting the act.

The data shown on your statement of account is shown by act and year or by act and period.

Amount debited column

We use the amounts shown in this column to calculate your total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are added to the balance you must pay.

Amounts followed by a minus sign (-) are subtracted from the balance.

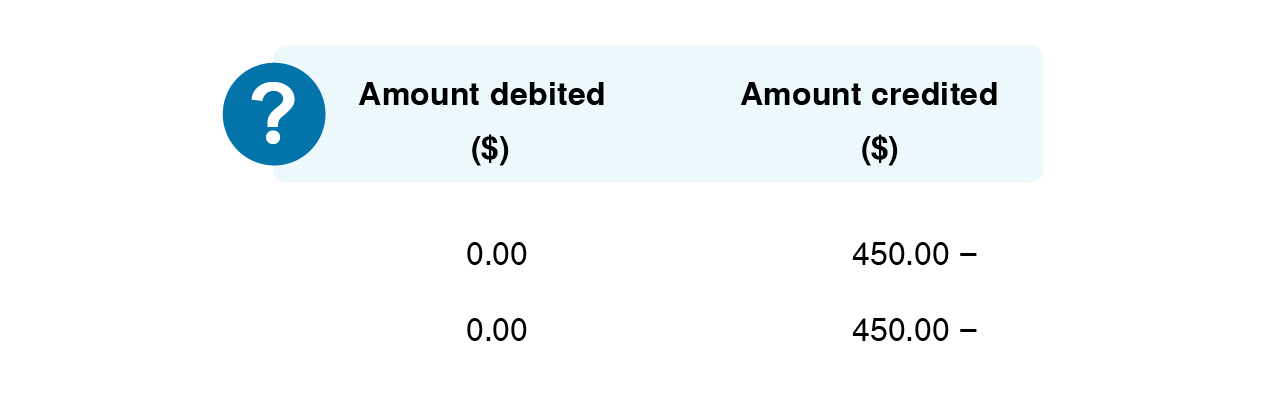

Amount credited column

This column has no direct bearing on the “Amount debited” column, and we do not include the amounts in it when calculating your total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are paid to you.

Amounts followed by a minus sign (-) reduce the balance of your “amount credited” to $0 if payments were made to you.

If you make instalment payments, they will be followed by a minus sign (-) and, when your notice of assessment is issued:

they will be deducted from your balance (personal income tax); or

they will be moved to the “Amount debited” column and deducted from your balance.

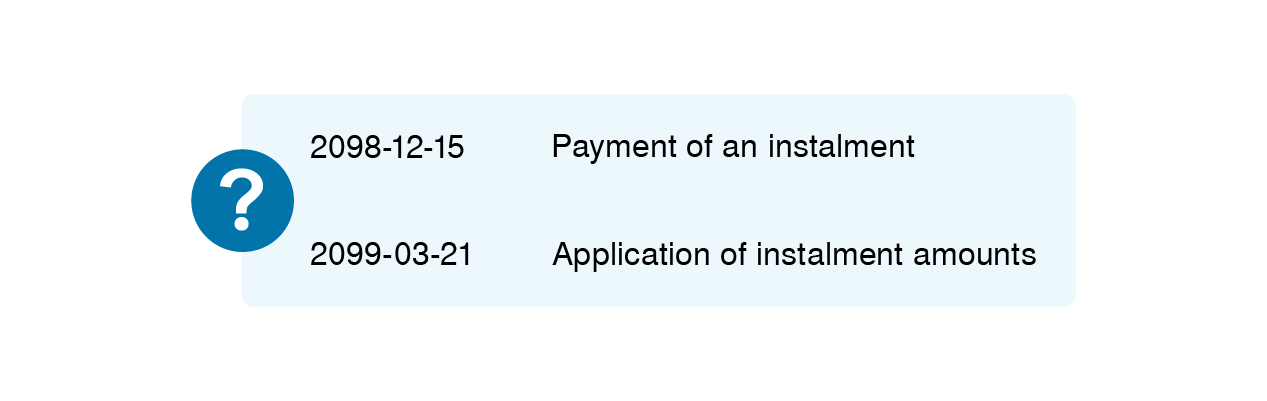

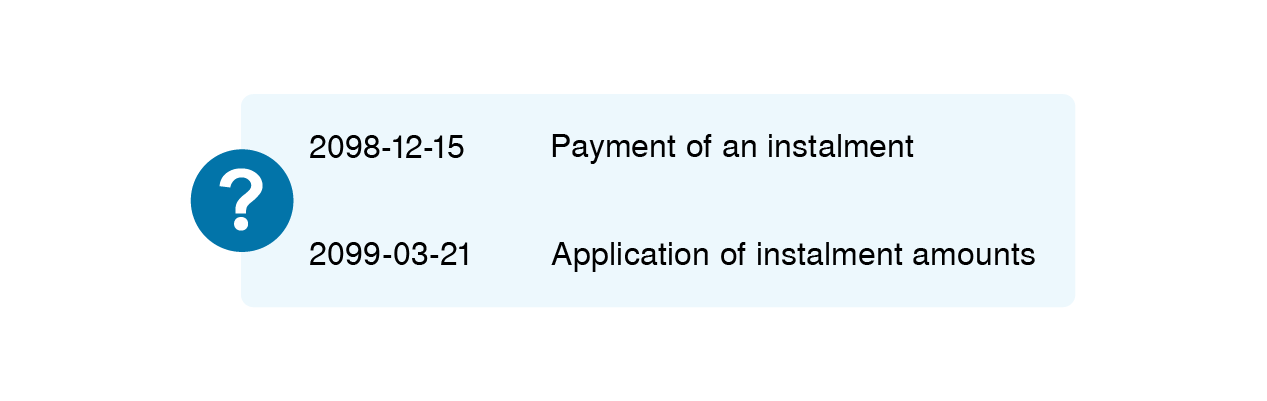

Payment of an instalment

Instalments of income tax, contributions and premiums and consumption taxes (GST/HST or QST) that you periodically remit to us.

Application of instalment amounts

The process of applying all instalment payments you've made for a given taxation year to the payment of your balance. We do this when we issue your notice of assessment for your income tax return. The process allows us to reduce your “amount credited” to zero.

“Application” is used in other accounting entries that may appear in a statement of account. Generally speaking, it means processing an amount to reduce the amount credited to zero.

Fee for management of tax collection or failure to file

Fixed fee charged to open your collection file.

Recovery charges

Fees charged to you if we have to take administrative or legal measures to collect an amount you owe us. The fees can be charged for each of the laws you're subject to.

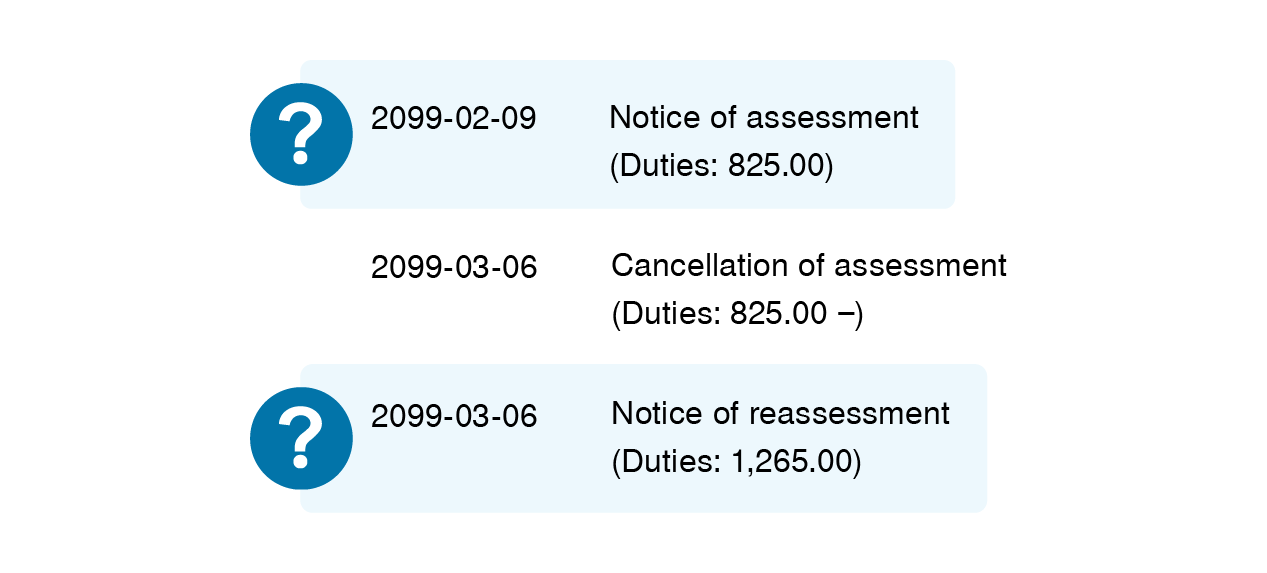

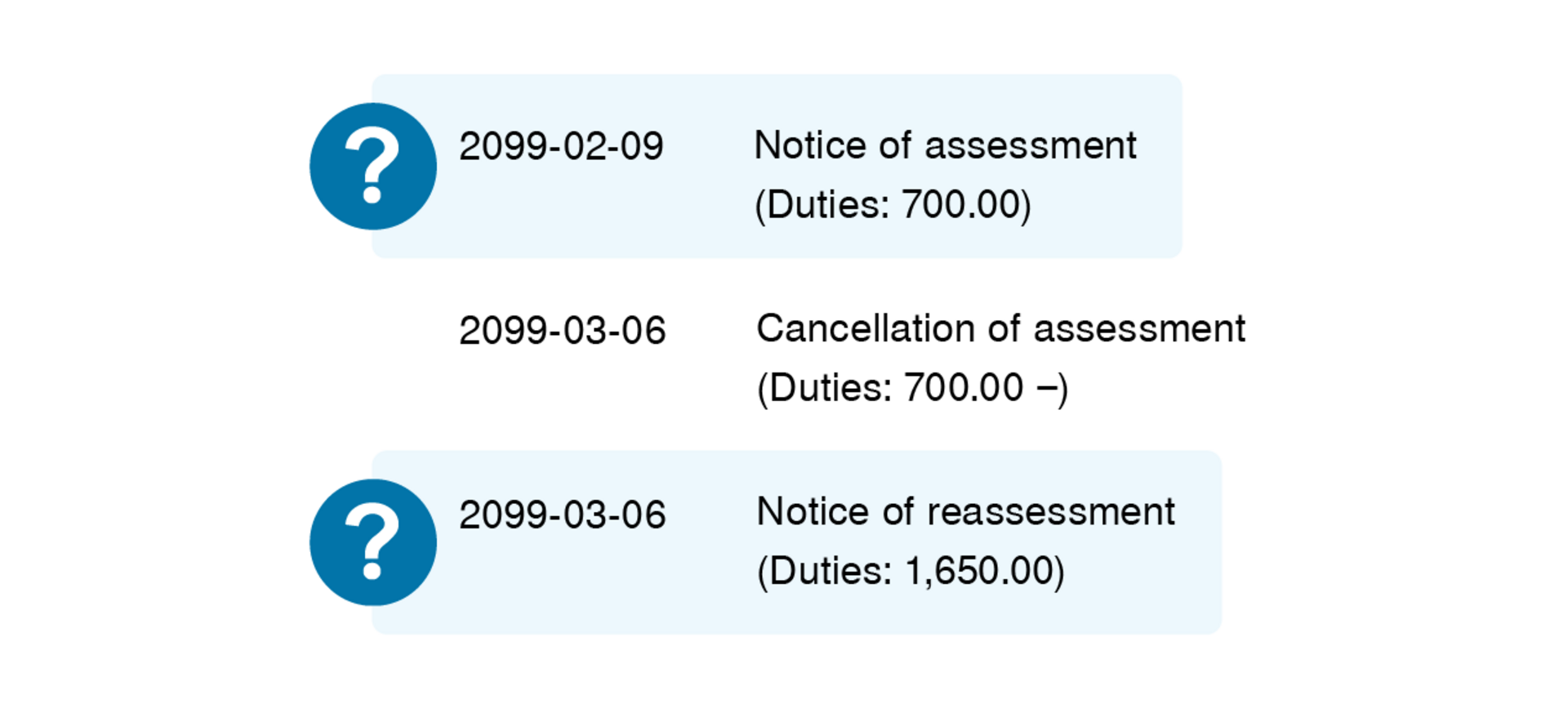

Notice of assessment

Paper or electronic document that we issue after reviewing an income tax, consumption tax or source deductions and employer contributions return you filed. The notice of assessment shows:

the calculation of income tax, consumption taxes or source deductions and employer contributions, and any interest and penalties you must pay for a given taxation year or period, as well as amounts you've already paid for the year or period

the balance you must pay or the refund you're entitled to for your return for the year or period

Notice of reassessment

Paper or electronic document that we issue, for example, after you make a request to change your income tax return or after your file was audited. The notice of reassessment amends your previous notice of assessment. It shows:

the revised calculation of income tax, consumption taxes or source deductions and employer contributions, and any interest and penalties that you must pay for a given taxation year or period, as well as amounts that you've already paid for the year or period

the adjusted balance you must pay or the adjusted refund you're entitled to for the return for the year or period

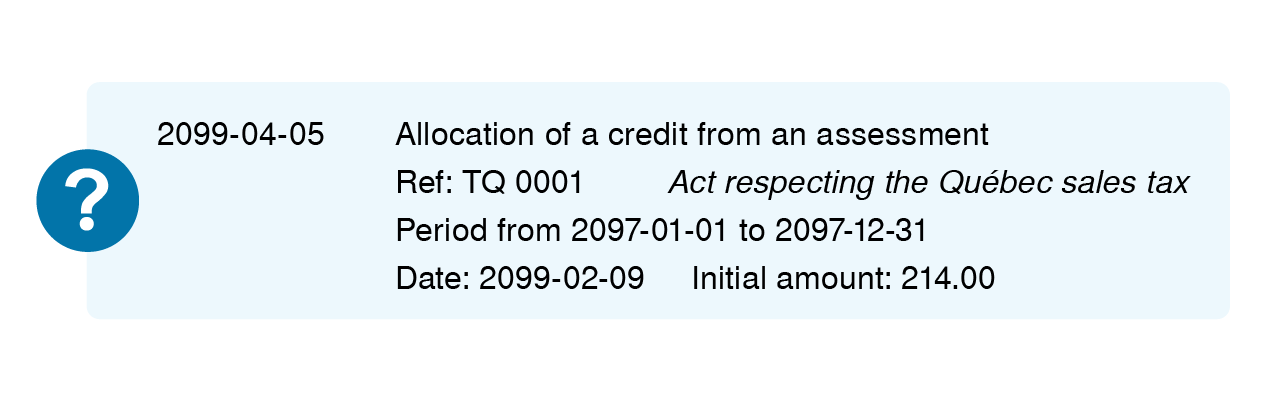

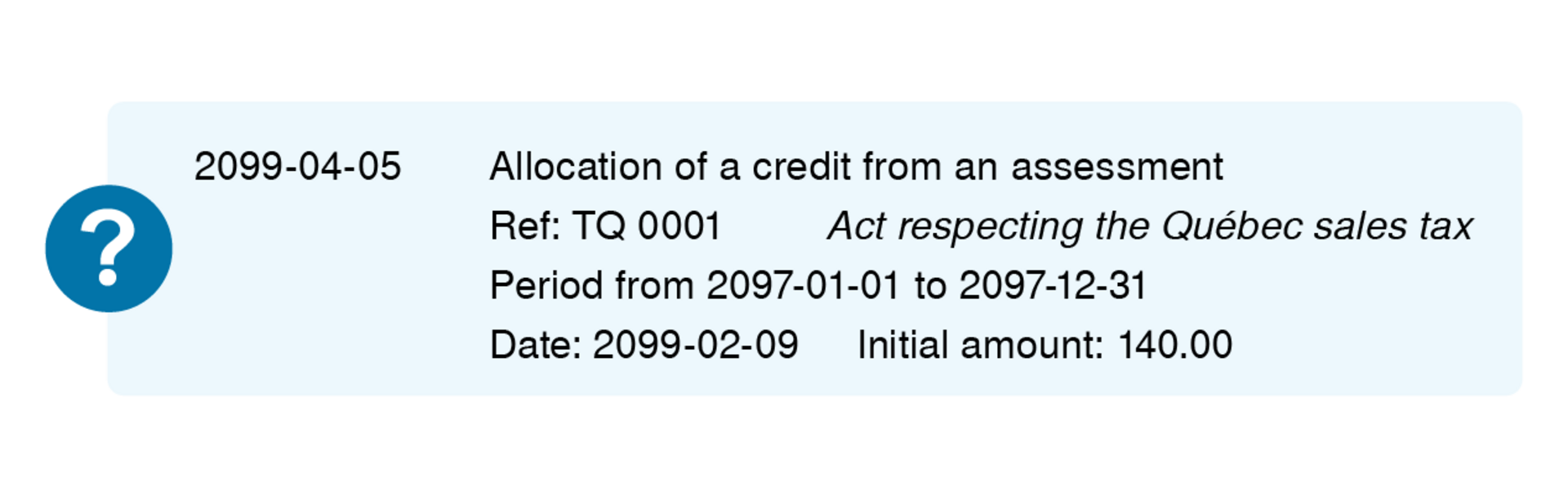

Allocation of a credit from an assessment

Use of a credit you were owed, after filing a return, to reduce or pay a debt you owe.

“Allocation” is used in other accounting entries that may appear in a statement of account. In all cases, it means use of an amount owed to you to reduce or pay a debt you owe.

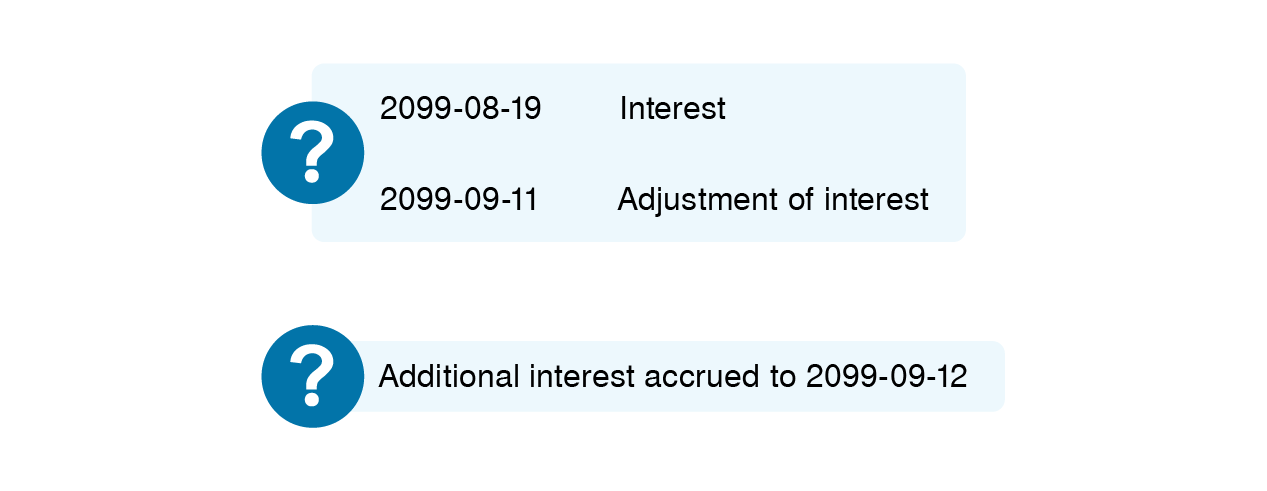

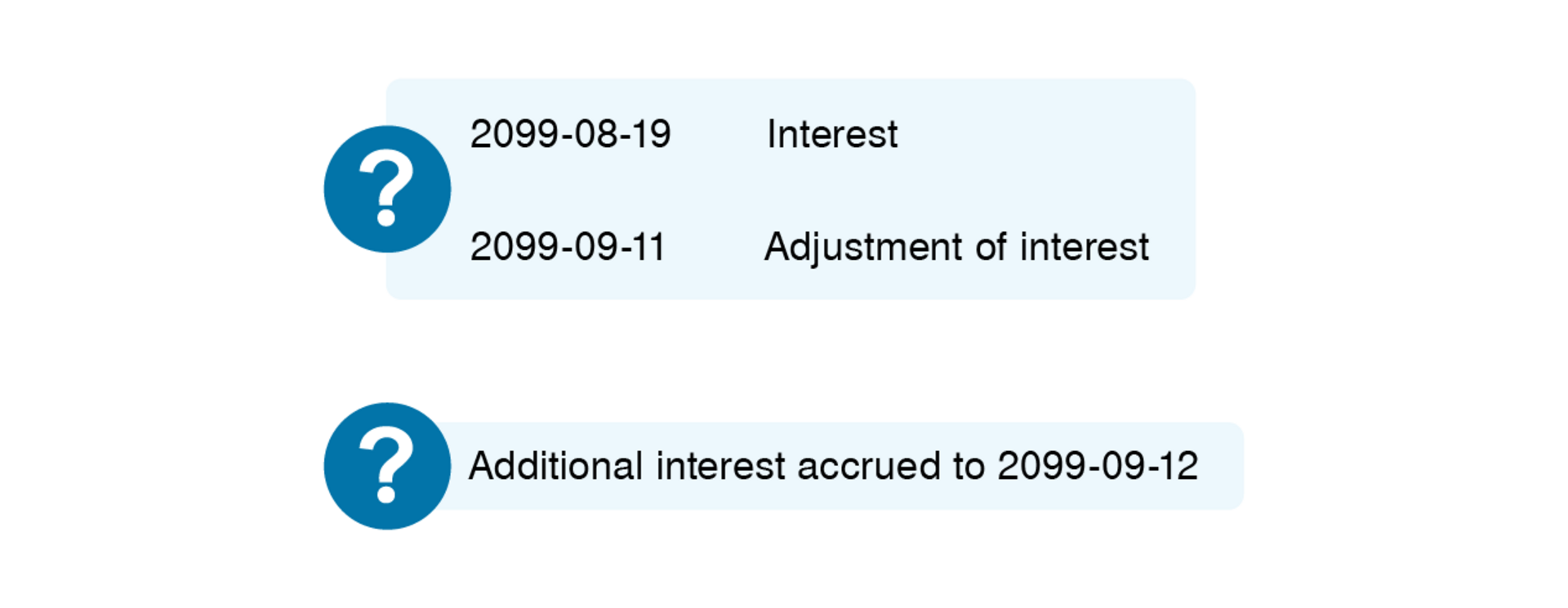

Interest

Amount added to your balance, at the rate set by law, for each day after the payment deadline.

Adjustment of interest

Recalculation of interest based on payment (partial or full) of your balance or application of a credit to the balance.

Additional interest

Additional interest added to the interest already calculated daily on the balance you haven't paid within the required timeframe.

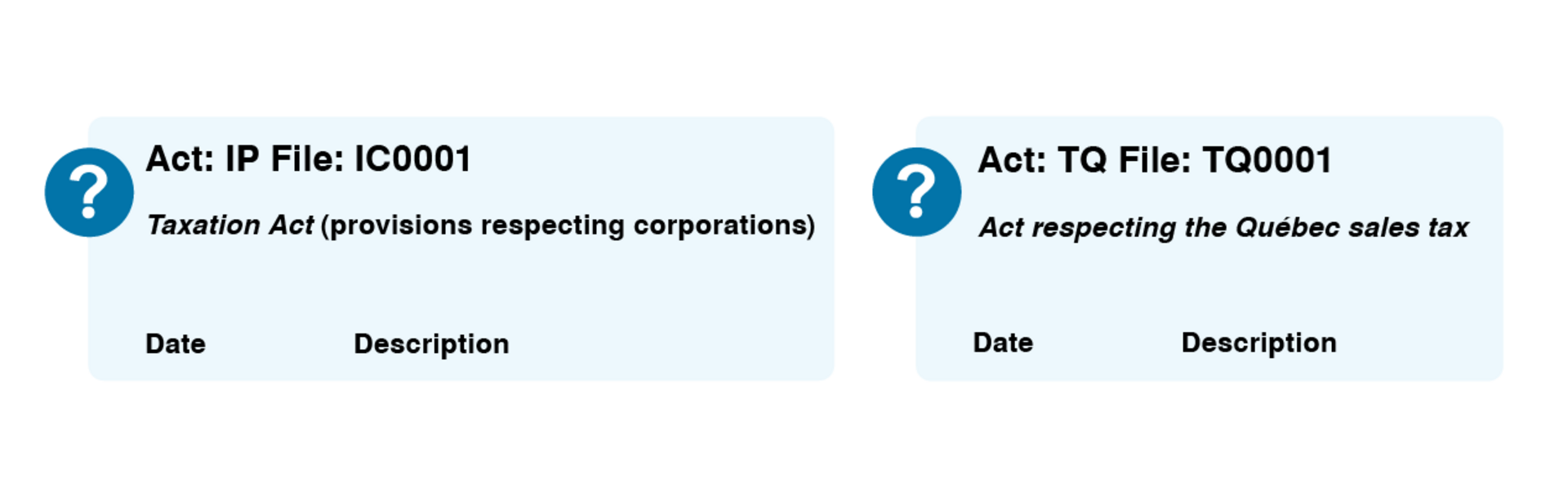

Statement of account sent to a corporation

Here's an example of a statement of account sent to a corporation. Click on the question mark for the information you want to see.

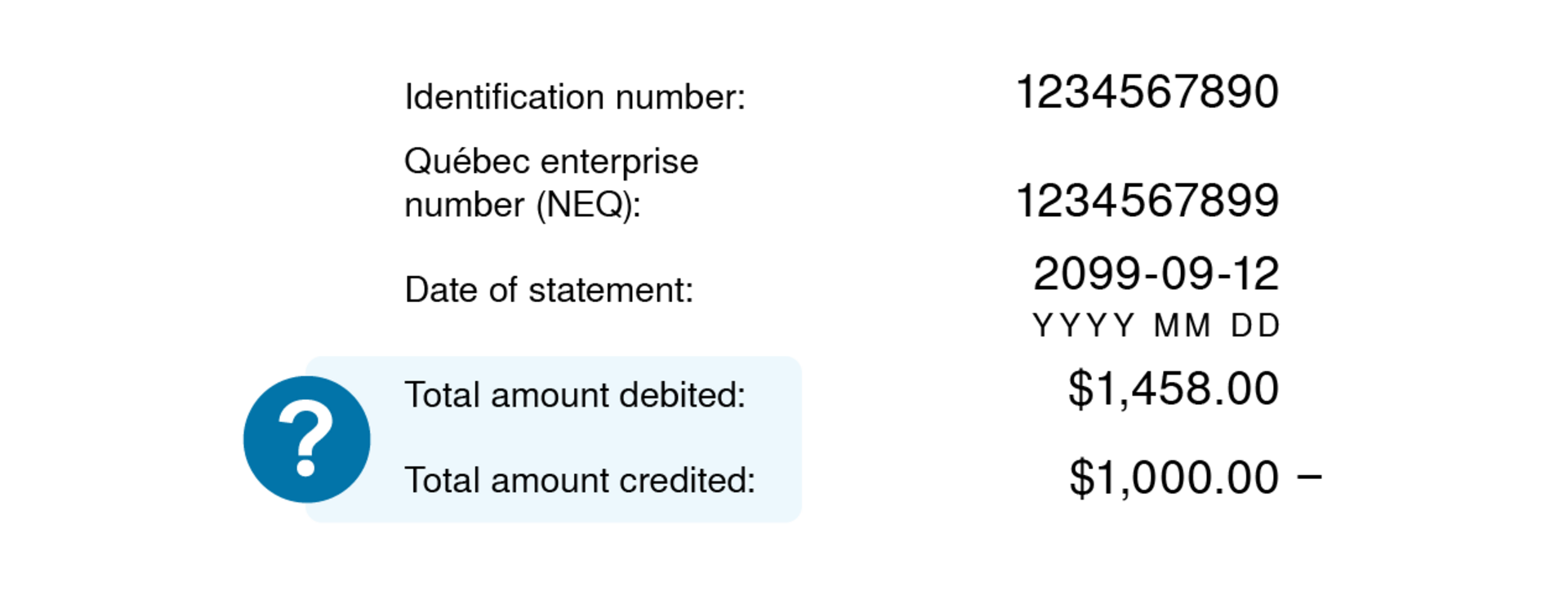

Total amount debited

Total balance to be paid by the corporation.

Total amount credited

Instalment payment amount that the corporation has remitted for its returns that we have not yet received or processed. This may also be an amount related to any other credit that was not yet accounted for, such as overpayments or a credit that was misallocated.

Although tax credits the corporation is entitled to are entered in the “Amount credited” column, they are not included in its total amount credited in the header.

Act, file number respecting the act and period or fiscal period

Act under which the corporation is required to pay a balance or is entitled to a refund, and file number respecting the act.

The data shown on the corporation's statement of account is shown by act and period or by act and fiscal period.

Amount debited column

We use the amounts shown in this column to calculate the corporation's total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are added to the balance the corporation must pay.

Amounts followed by a minus sign (-) are subtracted from the balance.

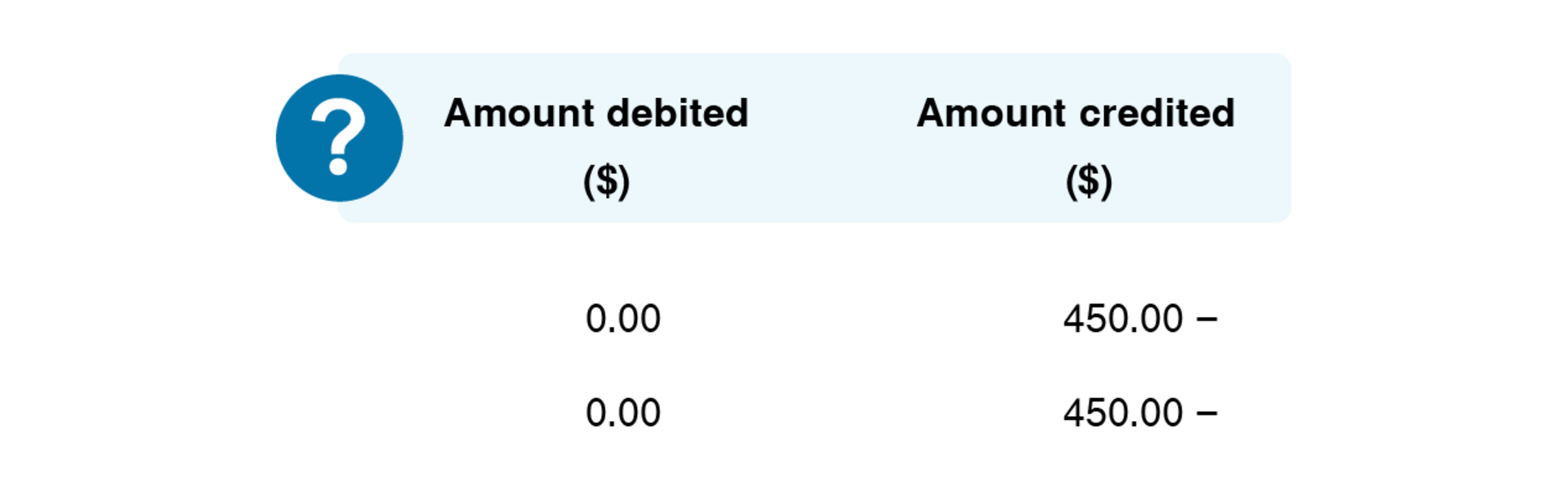

Amount credited column

This column has no direct bearing on the “Amount debited” column, and we do not include the amounts in it when calculating the corporation's total balance.

The following rules apply to this column:

Amounts without a minus sign (-) are paid to the corporation.

Amounts followed by a minus sign (-) reduce the balance of the corporation's “amount credited” to $0 if payments were made to the corporation.

If the corporation makes instalment payments, they will be followed by a minus sign (-) and, when its notice of assessment is issued, they will be moved to the “Amount debited” column and deducted from the total balance.

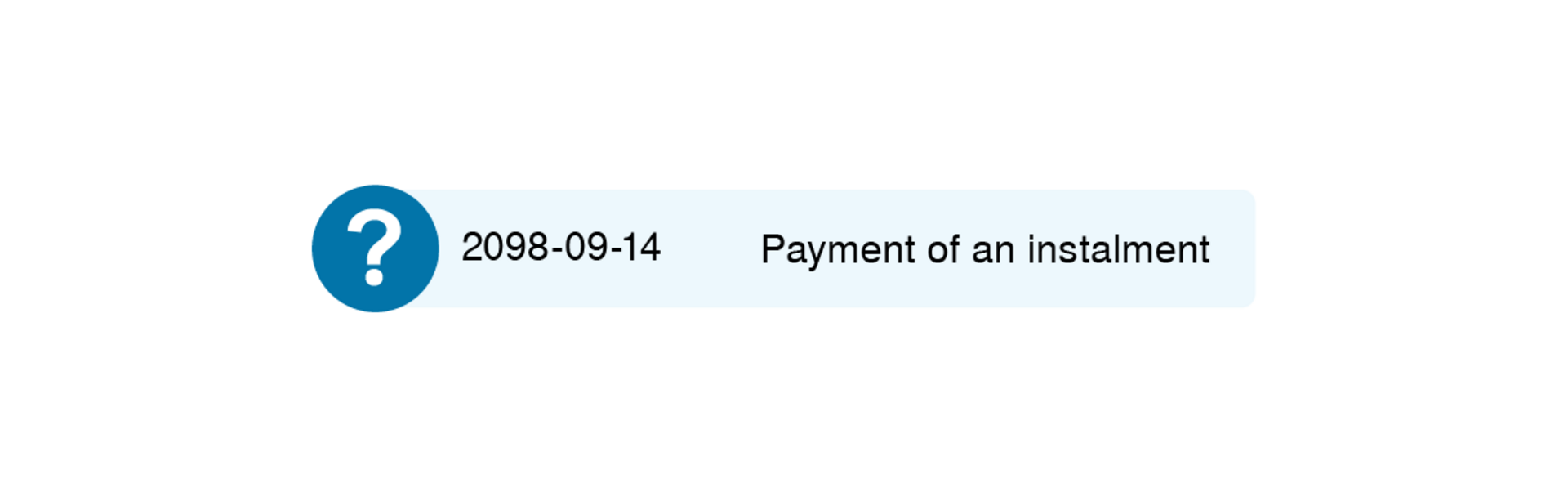

Payment of an instalment

Instalments of income tax, source deductions and employer contributions or consumption taxes (GST/HST or QST) that the corporation periodically remits to us.

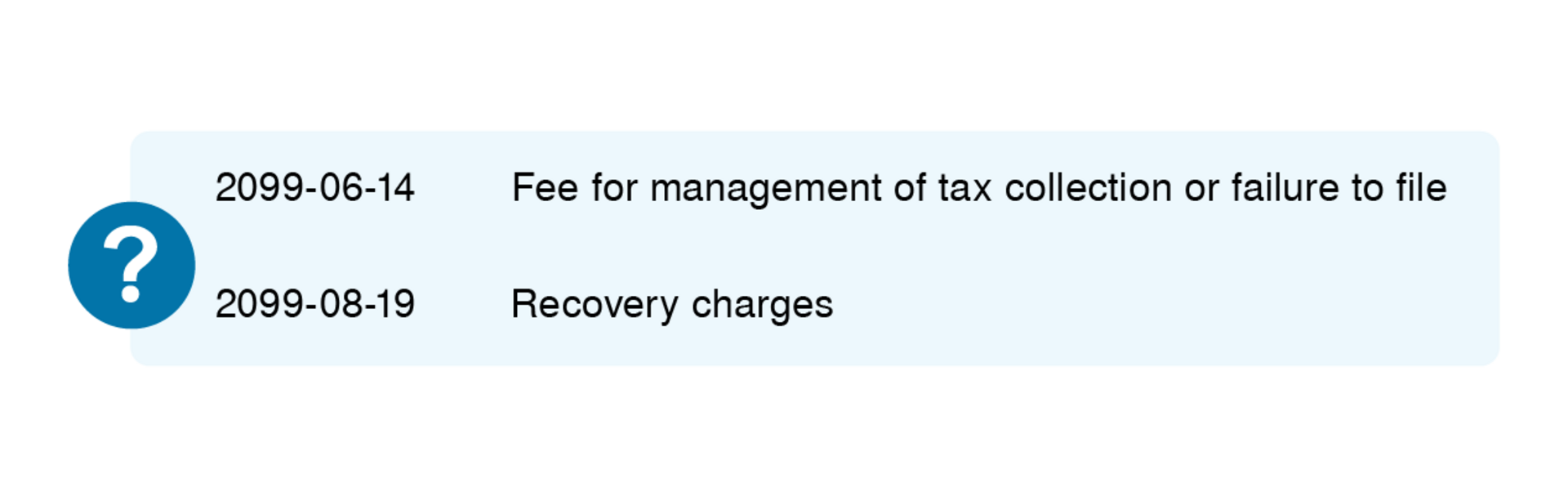

Fees for management of tax collection or failure to file

Fixed fees charged to open a corporation's collection file.

Recovery charges

Fees charged to the corporation if we have to take administrative or legal measures to collect an amount it owes us. The fees can be charged for each of the laws the corporation is subject to.

Notice of assessment

Paper or electronic document that we usually issue to a corporation after reviewing an income tax, consumption tax or source deductions and employer contributions return that it filed. The notice of assessment shows:

the calculation of income tax, consumption taxes or source deductions and employer contributions, and any interest and penalties that the corporation must pay for a given period or fiscal period, as well as amounts that it already paid for the period or fiscal period

the balance the corporation must pay or the refund it's entitled to for its return for the period or fiscal period

Notice of reassessment

Paper or electronic document that we issue to a corporation, for example, after it requests a revision of a return or after its file was audited. The notice of reassessment amends a previous notice of assessment. It shows:

the amended calculation of income tax, consumption taxes or source deductions and employer contributions, and any interest and penalties that the corporation must pay for a given period or fiscal period, as well as amounts that it already paid for the period or fiscal period

the adjusted balance the corporation must pay or the adjusted refund it's entitled to for its return for the period or fiscal period

Allocation of a credit from an assessment

Use of a credit owed to the corporation, after filing a return, to reduce or pay a debt the corporation owes.

“Allocation” is used in other accounting entries that may appear in a statement of account. In all cases, it means use of an amount owed to the corporation to reduce or pay a debt it owes.

Interest

Amount added to a corporation's balance, at the rate set by law, for each day after the payment deadline.

Adjustment of interest

Recalculation of interest based on payment (partial or full) of the corporation's balance or application of a credit to the balance.

Additional interest

Additional interest added to the interest already calculated daily on the balance the corporation has not paid within the required timeframe.