1. Introduction

This guide explains how to file the RL-22 slip (see courtesy translation RL-22-T) for employment income related to multi-employer insurance plans. The information it contains does not constitute a legal interpretation of Québec or federal laws and regulations.

This guide is for 2024 and subsequent years, unless administrative or legislative changes make a new version necessary.

For more information, contact us.

1.1 Legal references

References at the end of certain paragraphs are to sections of the Tax Administration Act (TAA, followed by section numbers), the Regulation respecting fiscal administration (TAA (r. 1), followed by section numbers), the Taxation Act (section numbers only), the Regulation respecting the Taxation Act (section numbers with the letter “R”) or the Act to establish a legal framework for information technology (ALFIT, followed by section numbers).

1.2. Definitions

Individual

A natural person covered (in whole or part) by a plan by reason of their:

- office or employment (past, present or future); or

- operation of a business, as a sole proprietor or as a member of a partnership.

Multi-employer insurance plan

A personal insurance plan that:

- applies to an economic sector, industry or activity (or subdivision thereof) under a law, regulation or government order;

- is offered jointly by employers operating in the same economic sector or industry, or engaged in the same activity; and

- is managed by one administrator.

Reference: 43.1

Construction-industry employee insurance plans are multi-employer insurance plans.

A medical care insurance plan or hospital care insurance plan (or both), or an insurance contract covering medical expenses, hospital expenses or any combination thereof, provided the plan or contract meets one of the following conditions:

- It covers only services or expenses that qualify for the non-refundable tax credit for medical expenses.

- It essentially covers services or expenses that qualify for the non-refundable tax credit for medical expenses, and the premium (or any other amount payable) for coverage is substantially attributable to such medical expenses.

A plan or contract established or provided for under provincial legislation to which the federal government contributes under fiscal agreements is not considered a private health services plan.

Reference: 1

- This definition includes group insurance plans that cover such services or medical expenses, as well as contracts and plans that provide full or partial coverage of dental or vision care expenses.

- To qualify as a private health services plan, a plan must involve one person agreeing to compensate another, for an agreed consideration, for a loss or liability related to an event that may or may not occur. If an employer has arranged to reimburse employees for expenses they or their dependants incur for medical, hospital or dental care, this arrangement may qualify as a private health services plan.

2. General information

2.1. Purpose of the RL-22 slip

The RL-22 slip (see courtesy translation RL-22-T) is used to report an individual's coverage under a multi-employer insurance plan (other than a plan covering total or partial loss of business, office-related or employment income).

Individuals use the RL-22 slip to complete their income tax return (TP-1-V).

2.2. Who must file RL-22 slips?

Administrators of multi-employer insurance plans must file RL-22 slips.

Reference: 1086R40

2.3. RL-22 slip recipients

An RL-22 slip must be filed for each individual:

- who was covered for the year by a multi-employer insurance plan (other than a plan covering total or partial loss of business, office-related or employment income);

- for whom, because of an office or employment, an employer paid contributions to the administrator of a multi-employer insurance plan for the year.

3. Filing the RL-22 slips

3.1. Filing methods

The required information must be provided on the prescribed RL-22 slip (see courtesy translation RL-22-T).

You must file the RL-22 slip using one of the following:

- authorized software you purchased;

- software you developed that meets our requirements;

- the fillable PDF you can download from our website;

- the paper slip you can order using our Ordering Forms and Publications online service or from our client services.

We do not provide financial compensation for providing your own slips.

3.2. Deadline for filing and distribution

On or before the last day of February in the year following the year covered by the RL slips, you must:

- file the RL-22 slips with Revenu Québec; and

- distribute copies of the RL-22 slips to the individuals.

References: 1086R65, 1086R70

3.3. Filing the RL slips with Revenu Québec

If you are filing more than 5 RL-22 slips, you must send them to us online (in an XML file) using software we have authorized.

If you are filing fewer than 6 RL-22 slips, you must send them to us either online (in an XML file) using software we have authorized or by mail (on paper). For paper RL slips, send us only copy 1 of each slip.

Do not send us copy 1 of the paper RL slips if you send us the slips online. However, make sure you keep the paper copies or electronic files.

Send documents that are not filed online to one of the addresses below:

| Montréal, Laval, Laurentides, Lanaudière and Montérégie | Revenu Québec C. P. 6700, succursale Place-Desjardins Montréal (Québec) H5B 1J4 |

|---|---|

| Québec City and other regions | Revenu Québec C. P. 25666, succursale Terminus Québec (Québec) G1A 1B6 |

For more information on filing RL slips, see the Tax Preparers' Guide: RL Slips (ED-425-V). For information on filing RL slips online using authorized software, contact the Division de l'acquisition des données électroniques at 418 659-1020, 1 866 814-8392 (toll-free) or [email protected].

References: 1086R65; TAA 37.1.1; TAA (r. 1) 37.1.1R1; ALFIT 3, 28, 29 and 71

3.4. Distributing RL slips to individuals

There are a number of options for distributing copies of the RL slips to individuals. If you distribute paper RL slips, you must give each individual copy 2 of the slip in person or send it to them by mail or by some other means. You can send the RL slip to an individual electronically, but only if you obtain the person's prior written consent (by mail, electronically or by some other means).

Individuals must clearly state that they consent to receiving the RL-22 slip electronically and that their consent will remain valid until they inform you of their intent to revoke it. Furthermore, you must inform them of how they can revoke their consent.

When you file RL slips electronically, you must:

- protect individuals' personal information;

- be able to check the identity of everyone who gives their consent; and

- make sure that the information on the RL-22 slips cannot be modified.

References: 1086R70; ALFIT 3, 28, 29 and 71

3.5. Amending or cancelling an RL slip

You can file an amended slip to replace a slip you have already filed that has one or more errors (e.g. an incorrect amount).

Do not file an amended slip for the following errors:

- the individual's address (in this case, make a duplicate of the original slip and send it to the individual only);

- the individual's social insurance number (SIN), first name or last name (in this case, you must cancel the RL-22 slip and make a new one).

A cancelled slip must be filed to replace a slip that should not have been filed or that has mistakes in the individual's SIN, first name or last name.

3.5.1. RL slip filed online (in an XML file)

To amend or cancel an RL slip that you have already filed online (in an XML file), follow the instructions in the Tax Preparers' Guide: RL Slips (ED-425-V). You can file amended or cancelled RL-22 slips online.

3.5.2. Paper RL slip filed by mail

To amend a paper RL slip sent by mail, file a new slip with the word “Modifié” on it and the letter “A” in the box marked “Code du relevé.” Enter the revised amounts in the appropriate boxes and re-enter the amounts from the other boxes of the slip that was previously filed. In the box marked “No du dernier relevé transmis,” enter the number shown in the upper right-hand corner of the slip you want to amend.

To cancel a paper RL slip that has already been filed, make a photocopy of the original slip, write “Annulé” on it and, in the box marked “Code du relevé,” enter the letter “D.” Make sure that the number shown in the upper right-hand corner of the original slip is legible on the photocopy.

3.6. Penalties

Under the Tax Administration Act, you are liable to a penalty if:

- You file an RL-22 slip late.

- You do not file online when filing more than 5 RL-22 slips.

If you fail to provide any required information on an RL-22 slip, you are liable to a penalty of $100. However, this penalty will not apply if the omission concerns the individual's personal information and you made reasonable efforts to obtain it.

References: TAA 59, 59.0.0.3, 59.0.0.4 and 59.0.2

4. Completing the RL-22 slip

4.1. Box marked “Année”

Enter the year in which the individual was covered by the multi-employer insurance plan.

4.2. Box marked “Code du relevé”

Enter “R” for an original slip, “A” for an amended slip and “D” for a cancelled slip.

4.3. Box marked “No du dernier relevé transmis”

Enter the number of the RL slip you want to change if you are completing an amended slip. For more information, see Amending or Cancelling an RL Slip.

4.4. Box A – Total value of the individual's coverage under a multi-employer insurance plan

Enter the total value of the individual's coverage under a multi-employer insurance plan (not including coverage for total or partial loss of business, office-related or employment income). The coverage must have been provided (in whole or part) because of the individual's:

- office or employment (past, present or future); or

- operation of a business, as a sole proprietor or as a member of a partnership.

Even if no premiums were paid with respect to the individual for the year, indicate the value of all of the individual's types of coverage that year.

Enter “0” in box A if the individual was not covered by the insurance plan but the employer paid premiums for them for the year.

To calculate the value of the individual's total coverage (all types) under a multi-employer insurance plan, determine the value of the individual's coverage under the private health services plan and add the value of the other types of coverage under a multi-employer insurance plan (for example, life insurance, insurance covering accidental death, or accident insurance covering bodily injury).

In addition to being included in the amount in box A, the value of the individual's coverage under the private health services plan must be entered in box B.

The following sections explain how to calculate the value of the various types of coverage provided to individuals, according to whether or not the plan is backed by an insurance contract.

4.4.1. Plan not backed by an insurance contract

Where coverage under a plan is not backed by an insurance contract underwritten by an insurance corporation, the value of the coverage is equal to the amount by which the value of the coverage exceeds the individual's total contributions to the plan during the year.

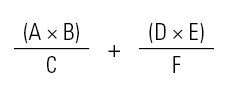

The following formula is used to calculate the value of the coverage:

The total benefits (including taxes) paid during the year to all employees who had the same types of benefits and coverage as the individual, multiplied by the number of days in the year during which the individual enjoyed the benefits and coverage concerned, divided by the total number of employees who had the benefits and coverage for each day in the year

plus

The total expenses (and related tax) charged by a third party for plan administration or management for the year, multiplied by the number of days in the year during which the individual was covered by the plan, divided by the total number of employees covered by the plan, for each day in the year

Definition of variables

- A = Total benefits (and related tax) paid during the year to all employees who had the same types of benefits and coverage as the individual concerned (for private health services plans, see Services insured by the Régie de l'assurance maladie du Québec)

- B = Number of days in the year during which the individual enjoyed the benefits and coverage concerned

- C = Number of employee-days of coverage (that is, the total number of employees who had the types of benefits and coverage concerned, for each day in the year)

- D = Expenses (and related tax) charged by a third party for plan administration or management for the year

- E = Number of days in the year during which the individual was covered by the plan

- F = Number of employee-days of coverage under the plan (that is, the total number of employees covered by the plan, for each day in the year)

If optional benefits (for example, coverage of medical, hospital or dental expenses) or different types of coverage (such as individual, single-parent or family) are available under a plan, and employee benefits and coverage differ, apply the formula (A × B) ÷ C to each type of benefit the individual has.

When calculating the value of an individual's coverage, if a plan does not distinguish between types of benefits and coverage, do not break down the benefits paid under the plan according to whether or not employees' families were covered or according to whether or not employees were reimbursed for certain types of expenses.

For more information on how to calculate the value of an individual's coverage, see the guide Taxable Benefits (IN-253-V).

Reference: 37.0.1.4

4.4.1.1. Expenses incurred for plan administration or management (variable D)

Only expenses charged by a third party can be used to calculate the value of the individual's coverage. Such expenses do not include the cost of establishing or amending the plan (for example, fees paid to obtain professional advice, or other costs related to plan establishment or amendment).

4.4.1.2. Stop-loss insurance (variable A or D)

The benefits paid under a stop-loss insurance contract (a contract under which an insurer undertakes to cover losses beyond a certain amount for a given period) must not be included in total benefits paid under the plan (variable A).

However, the insurance premiums (and related tax) that you, as plan administrator, paid under a contract for the year must be taken into consideration in determining the value of the individual's coverage under an insurance plan for which you have taken out a stop-loss insurance contract. If the stop-loss insurance applies to all types of benefits and coverage provided under the plan, the insurance premiums (and related tax) that you paid must be included in variable D. If the stop-loss insurance applies only to certain specific types of benefits or coverage, the insurance premium (and related tax) must be included in variable A (for benefits or coverage provided by the stop-loss insurance).

4.4.2. Plan backed by an insurance contract

If coverage under a plan is backed by an insurance contract underwritten by an insurance corporation, the value of the coverage equals:

- the total premium (and related tax) paid for the individual's benefits and coverage for the year (for private health services plans, see Services insured by the Régie de l'assurance maladie du Québec);

minus

- the total of:

- the amount reimbursed by the individual during the year; and

- the dividends, returns or refunds of premiums (and related tax) that you received, as plan administrator, during the year in relation to the individual's benefits and coverage.

4.4.2.1. Benefits or types of coverage under the insurance contract

If an insurance contract is related to a multi-employer insurance plan, other than a private health services plan, and offers various types of benefits (for example, basic life insurance, supplementary life insurance, insurance covering accidental death, accident insurance covering bodily injury or basic health insurance), and the individual's premium is determined by the type of benefits offered, the value of the coverage corresponds to the premium (and related tax) paid for the specific type or types of benefits provided to the individual. Any amount paid by the individual for those benefits must be subtracted from the value of the coverage to be included in the amount in box A, provided the amount was paid in relation to an office or employment.

If an insurance contract is related to a private health services plan that offers more than one type of coverage (for example, individual, single-parent or family), with or without different types of optional benefits (such as coverage of medical, hospital or dental expenses), and the individual's premium is determined by a specific type of coverage or benefits, the value of the coverage is equal to the premium (and related tax) paid for the individual's type of coverage or benefits. Any amount paid by the individual during the year must be subtracted from the value of the coverage to be included in the amount in box A, provided the amount was paid in relation to an office or employment.

4.4.2.2. Dividend, return or refund of premiums

If, during the year, you receive a dividend, return or refund of premiums (hereinafter referred to as a “refund”) based on all of the types of benefits and coverage provided under the insurance contract, the portion of the refund (including related tax) related to the premium paid for an individual must be subtracted from the value of the coverage to be included in the amount in box A.

The portion of such a refund to be subtracted from the value of the coverage is calculated as follows:

The total refunds received by the plan administrator (other than the employees' share in the cost of the plan distributed to them), multiplied by the premium paid for the individual, divided by the premium paid for all employees

If the refund (including related tax) is based only on certain types of benefits and coverage provided under the insurance contract, the refund is divided only among those individuals who have the type of benefits or coverage concerned.

If you distribute, among individuals, the portion of the refund that corresponds to their share in the cost of the plan, the amount received by the individuals must not be included in their income from an office or employment.

Reference: 37.0.1.3

4.4.3. Services insured by the Régie de l'assurance maladie du Québec

4.4.3.1. Coverage backed by an insurance contract

If coverage under a private health services plan is backed by an insurance contract underwritten by an insurance corporation, exclude the portion of the premium paid for an individual that reasonably represents the cost that would be paid by the Régie de l'assurance maladie du Québec (RAMQ) for equivalent services insured under the Health Insurance Act.

However, if for a given period in the year, an individual is not subject to the Health Insurance Act (as in the case, for example, of an employee posted outside Canada), and if the private health services plan provides benefits and coverage that include at least all of the services for which the individual would be covered under the Act if they were subject to its provisions, subtract the prescribed amount under the Regulation respecting the Taxation Act from the premium paid for the individual for coverage during the period in question and reduce the related tax on insurance premiums accordingly.

The prescribed amount is obtained by multiplying $2.74 (for individual coverage) or $10.96 (in all other cases) by the number of days in the period concerned.

References: 37.0.1.2, 37.0.1.2R1

4.4.3.2. Coverage not backed by an insurance contract

If coverage under a private health services plan is not backed by an insurance contract underwritten by an insurance corporation, you must, in determining the value of the individual's coverage, exclude from variable A the amount of benefits that can be considered to relate to the cost that would be assumed by the RAMQ for services insured under the Health Insurance Act.

However, if for a given period in the year an individual is not subject to the Health Insurance Act (as in the case, for example, of an employee posted outside Canada), and if the private health services plan provides benefits and coverage that include at least all of the services for which the individual would be covered under the Act if they were subject to its provisions, subtract the prescribed amount under the Regulation respecting the Taxation Act from the individual's total benefits (variable A) for the benefits and coverage in question and reduce the related tax accordingly.

The prescribed amount is equal to the total of the amounts obtained by multiplying, for each such individual, $2.74 (for individual coverage) or $10.96 (in all other cases) by the number of days the individual is in this situation and benefits from the specific type of benefits and coverage in question.

References: 37.0.1.5, 37.0.1.5R1

4.5. Box B – Value of coverage under a private health services plan

Enter the value of the individual's coverage under a private health services plan. The coverage must have been provided (in whole or part) by reason of the individual's:

- office or employment (past, present or intended); or

- operation of a business, as a sole proprietor or as a member of a partnership.

This amount must also be included in the amount in box A and must be calculated as stipulated in Plan not backed by an insurance contract, or in Plan backed by an insurance contract.

The value of the coverage provided to a self-employed person under a private health services plan must also be entered in box B and be included in the amount in box A.

4.6. Space marked “Périodes de protection dans l'année”

Enter the periods the individual was covered by the private health services plan and received the value of a benefit included in the amount in box B.

4.7. Identification

4.7.1. Space marked “Nom de famille, prénom et adresse du particulier”

Enter the individual's last name, first name and last known address, including the postal code.

Also enter the individual's SIN.

Individuals must provide their SIN to any person required to file an RL slip in their name. Individuals who do not have a number must contact Service Canada to obtain one. The law also requires the person who completes and files the RL slip to make a reasonable effort to obtain the number from the individual. Omitting the SIN may result in a penalty for both the individual and the person required to file the slip.

4.7.2. Space marked “Nom et adresse de l'administrateur du régime”

Enter the multi-employer insurance plan administrator's name and address (including the postal code) on each RL-22 slip.

4.7.3. Space marked “Numéro de référence (facultatif)”

You can include a reference number to further identify the individual. This is optional.