RL-18 Slip

If you made securities transactions during the year, such as the sale of shares of publicly traded corporations, mutual fund units or bonds, your securities trader or dealer (such as your financial institution) must send you a prescribed form listing the transactions that you must report in your income tax return. All security transactions must be reported, even if the amount of the transactions is zero or negative.

You may receive:

- an RL-18 slip for each securities transaction you made during the year

- a form (the “consolidated T5008/RL-18 form”) that includes a federal T5008 slip, an RL-18 slip and one or more pages entitled “Securities Transactions Details” giving information about the securities transactions you made during the year

The RL-18 slip includes the information you need to complete your provincial income tax return, while the consolidated T5008/RL-18 form includes the information you need to complete both your provincial and federal income tax returns.

You are required to report your securities transactions even if you did not receive a consolidated T5008/RL-18 form or RL-18 slip from your securities trader or dealer. In this case, you must use the T5008 slip to complete your provincial return.

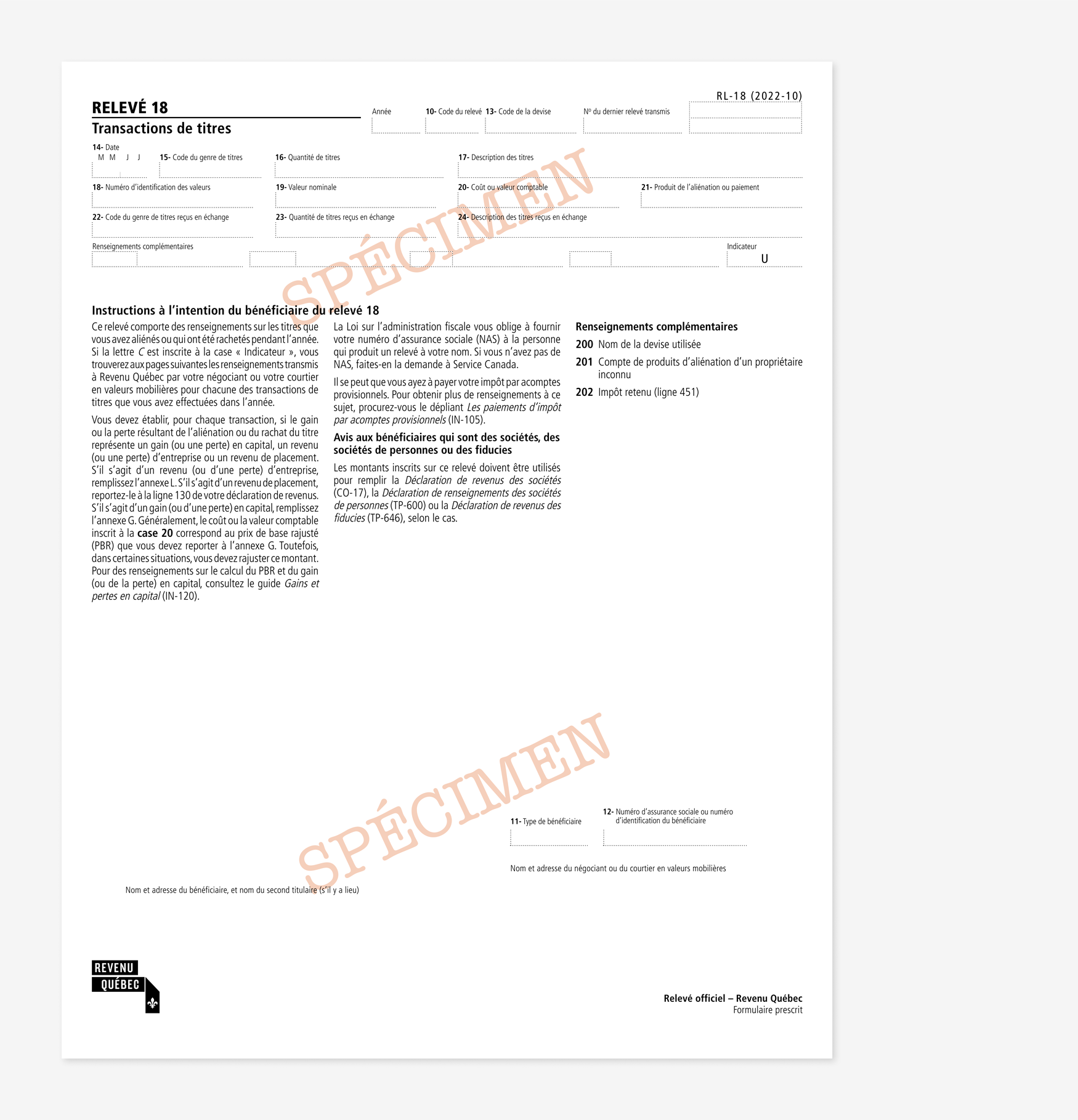

RL-18 slip – Single securities transaction

If you receive an RL-18 slip for each transaction during the year:

- The letter “U” is entered in the box marked “Indicateur.”

- Transaction information is shown is boxes 14 to 21.

The slip generally has only one page.

RL-18 slip showing information for a single securities transaction

RL-18 slip (single securities transaction)

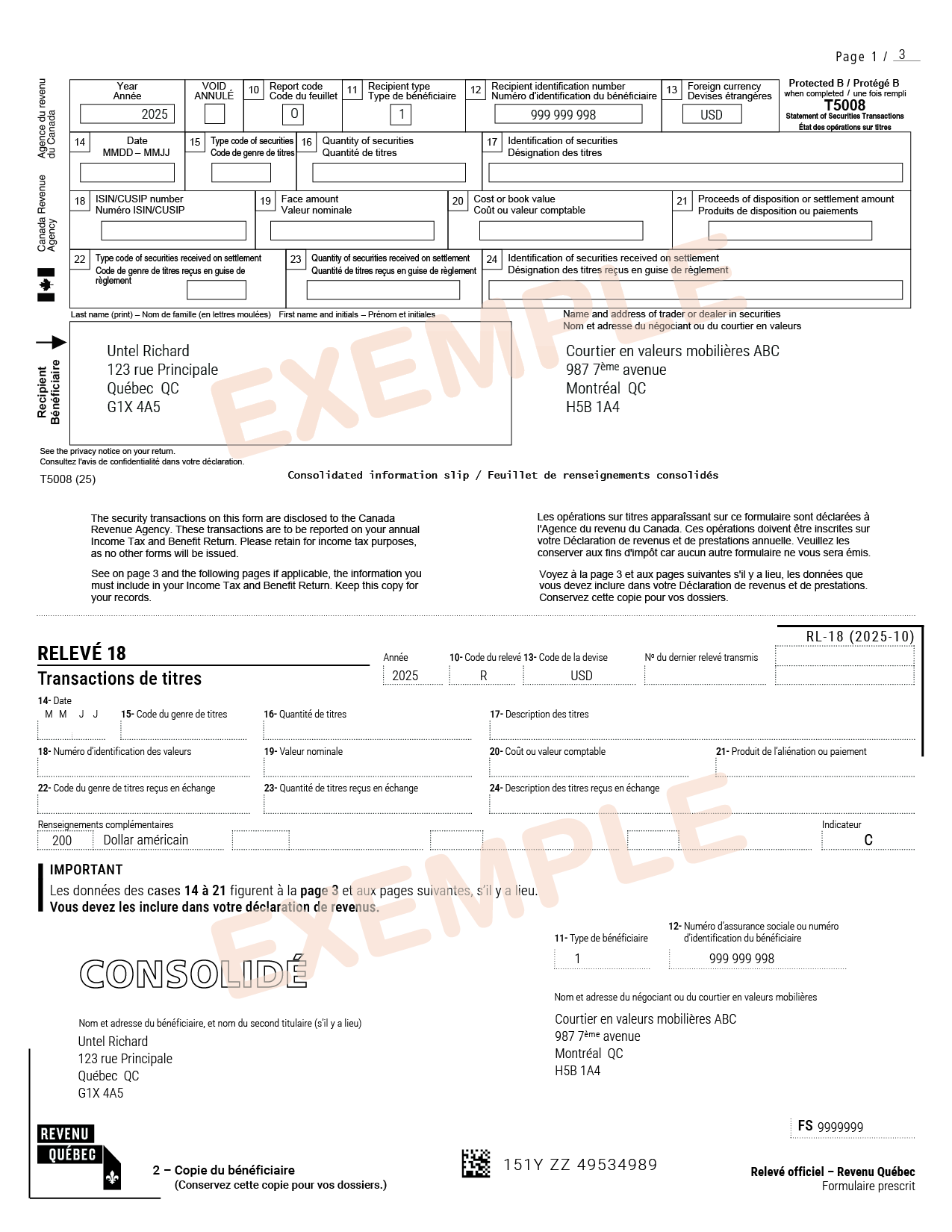

Consolidated T5008/RL-18 form – Multiple securities transactions

If you receive a consolidated T5008/RL-18 form, which will have information for multiple securities transactions:

- The letter “C” is entered in the box marked “Indicateur” of the RL-18 slip.

- The RL-18 slip includes the note “Consolidé.”

- Boxes 14 to 21 of the RL-18 slip are blank since the information about your securities transactions during the year is shown in the “Securities Transactions Details” table.

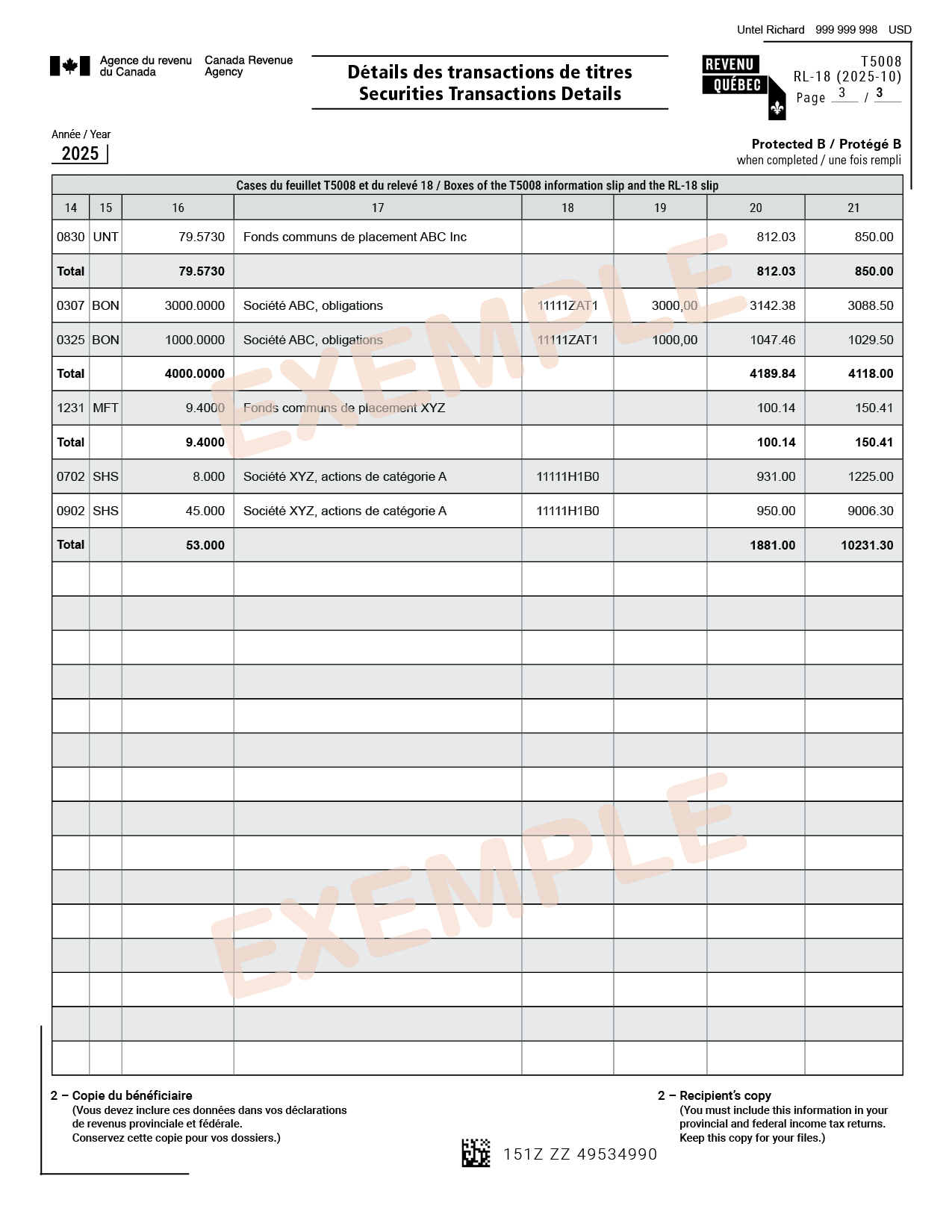

The consolidated T5008/RL-18 form has at least three pages. There is no total on pages 1 and 3 because the tax treatment of the transactions to report (capital gains, interest income, business income, etc.) depends on the nature of the securities sold (shares, bonds, linked notes, etc.). Since page 3 may list more than one kind of security, a total could be misleading.

However, to help you file your income tax returns, there is space on page 3 for your trader or dealer to enter subtotals for identical securities (for example, units in a single mutual fund, futures contracts on merchandise or shares of the same class of a corporation).

The information for boxes 14 to 21 is on page 3 and any additional pages. It must be included in your income tax return.

Consolidated T5008/RL-18 form

Page 1: T5008 slip and RL-18 slip

Page 2: Instructions for T5008 slip and RL-18 slip recipients

Page 3 and following: Securities Transactions Details table

How to meet your tax obligations

Step 1 – Gather your documents

Make sure you have the necessary document(s) (see the partial list below) from your securities trader or dealer for each securities transaction:

- an RL-18 slip giving information about a single securities transaction during the year

- a consolidated T5008/RL-18 form giving information about multiple securities transactions during the year

- an account or transaction statement

- any other document

Step 2 – Determine the amounts to report

For each transaction, determine the type of amount you are reporting, such as:

- business income or a business loss (i.e. income or loss from a commercial activity)

- a capital gain or loss

- interest or other investment income

To determine whether an amount is business income or a business loss rather than a capital gain or loss, see Part 2 of guide IN-155-V, Business and Professional Income.

If you are reporting a capital gain or loss, you must calculate it using the adjusted cost base (ACB) of the securities. The amount entered in box 20 of the RL-18 slip or on another document provided by your securities trader or dealer is not necessarily the ACB.

To calculate the ACB, you have to check whether the amount shown in box 20 or the amount on your supporting document takes into account capital repayments received for the current year and previous years. To check if it does, see:

- the documents sent by your securities trader or dealer

- guide IN-120-V, Capital Gains and Losses

Step 3 – Enter the amounts calculated in Step 2 in your income tax return

Enter the amount calculated for each transaction in Step 2 in your income tax return.

For information on how to report securities transactions and for instructions concerning the following lines of the income tax return, see the guide to the income tax return (TP-1.G-V):

Fixing your tax situation

If you have already filed your return and want to change it, see Correcting an Error or Omission.

If you failed to report securities transactions in the past, see our voluntary disclosure policy on fixing your tax situation.